Is JCB's Case Against China Built on Thin Air?

In international trade, a single chart can trigger millions of pounds in new taxes. That’s exactly what JCB is banking on right now, as it tries to persuade the UK’s Trade Remedies Authority to double the duties on Chinese excavators. Their argument? The Chinese are gaming the system by quietly absorbing the cost of existing tariffs rather than passing them on to buyers.

Dig beneath the surface of JCB’s application, though, and the picture gets murkier. A closer look at the data throws up several red flags — and some pretty compelling alternative explanations.

1. The Weight Trap

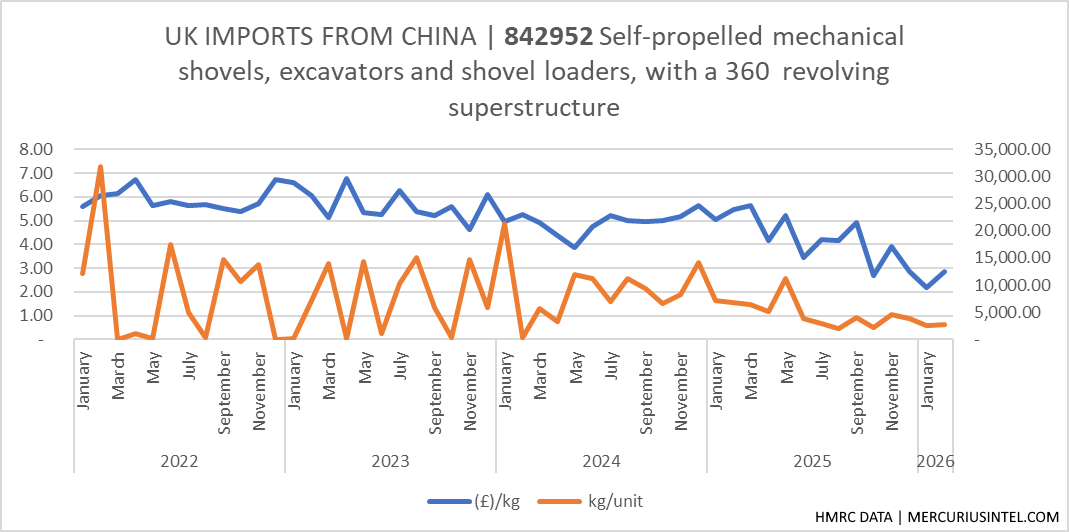

JCB’s entire case rests on a striking 20% fall in the average price per kilogram of Chinese imports. That sounds damning. But there’s a catch: the machines themselves are getting smaller.

Since the duties came in, the average weight per imported unit has dropped sharply. And in trade terms, that matters enormously. A 5-tonne mini-digger is inherently cheaper per kilo than a 20-tonne heavy excavator — not because anyone’s subsidising it, but because it’s a simpler machine. If UK buyers have quietly shifted toward smaller equipment, the price-per-kilo figure falls on its own, with no “absorption” required.

JCB insists this isn’t what’s happening. But their own charts show a dramatic dip in February 2025 that they breeze past without much explanation.

2. The Timeline Problem

Look carefully at the evidence JCB submitted and the timelines don’t quite line up.

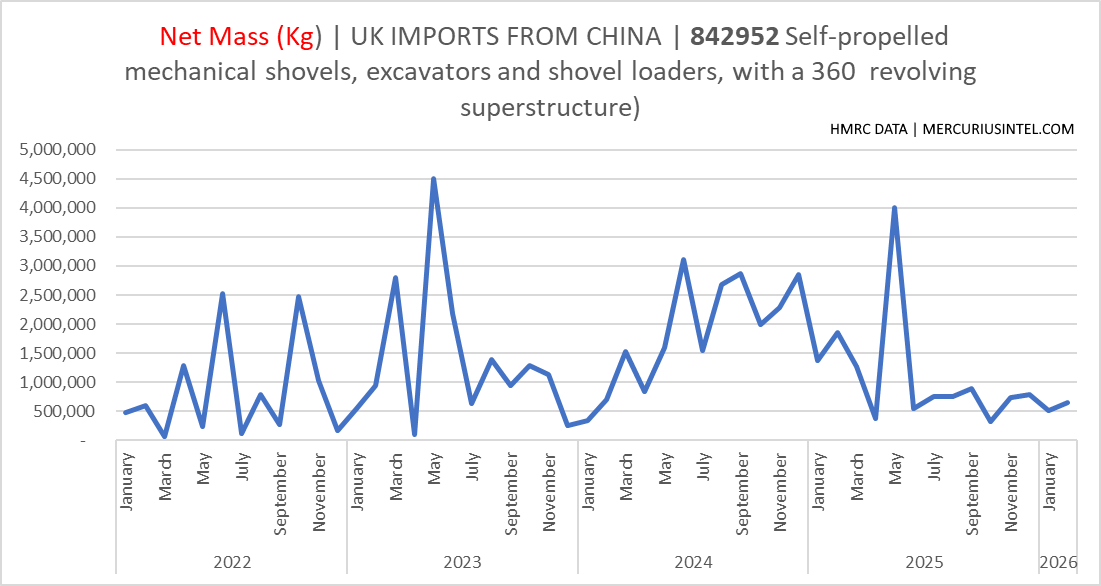

Their price chart runs all the way back to 2022, tracing a long and dramatic decline. Their volume chart, on the other hand, only starts in 2023. That gap matters. If import volumes in 2022 were significantly higher than they are today, what JCB is calling “stable” imports might actually represent Chinese exporters losing ground — not holding firm. Choosing where to start a chart is one of the oldest ways to shape a story rather than simply tell it.

3. Intelligence vs. Evidence

JCB has managed to get hold of a SANY price list, which gives them something solid to point to. But for other major players — Caterpillar, LiuGong, XCMG — much of the case rests on “market intelligence” and inference. They claim Caterpillar cut prices by as much as 20% in 2025, but the main evidence they cite for this is the same HMRC average that may already be skewed by the shift toward lighter machines. It’s a circular argument dressed up as corroboration.

4. What’s Actually Going On?

JCB frames the current situation as a “mockery” of UK trade law and is pushing for duties as high as 80.2% on some producers. Before the TRA goes anywhere near that number, it needs to answer one honest question: is China really swallowing the tariff to keep prices competitive — or did the UK market simply start buying smaller, cheaper machines to sidestep the heavier duties in the first place?

Those two scenarios look identical in the data. But they call for very different responses.

In a trade dispute, the party that draws the chart often gets to write the narrative. The question is whether the TRA looks closely enough to notice when the chart isn’t showing the whole picture.